If you’re a football fan, you know how important the red zone is for your favorite team. It’s the area on the field that requires a higher level of execution but leaves you with a smaller margin for mistakes. The success you have in the red zone often determines whether or not you win the game.

Much like the game of football, retirement planning has a similar period of time where it’s essential for your long-term success. We call this the Financial Red Zone, and it’s the 5-10 years prior to retirement and the first years in retirement. Planning and execution become critical during this time and we’ll tell you why on this episode.

Here’s some of what you’ll learn on the podcast:

- What is the Financial Red Zone? (2:01)

- How you should manage your risk during this time. (4:47)

- Every retirement plan should have these three types of money. (7:15)

- Why being proactive with your finances will benefit you in the red zone. (10:01)

- The experience we have working with people in this age range. (11:18)

If you have any questions, you can contact us online here: https://cravitzfinancial.com/

Take advantage of our free Retire Ready Checkup to get an assessment on where you stand: https://cravitzfinancial.com/retire-ready-checkup/

Full Transcript:

Ryan: So what if that affects the long term money? That's okay, as long as everything is put together and we know exactly when we're going to get our income from what sources, and when.

Announcer: When it comes to financial planning, you need to cut through the jargon so that you can understand how to achieve your own retirement success. This is Candid Conversations Retirement Talk with Ryan Cravitz of Cravitz Financial and Insurance Solutions.

Ben: Well, hello and welcome into Candid Conversations Retirement Talk with Ryan Cravitz. I am Ben George. Good to have you on the show today, Ryan. Are you a football fan?

Ryan: A little bit. I watched the LA Sports teams a little bit like I got into the Rams certainly last year. That was fun to watch and I'll always watch in the playoffs.

Ben: Yeah, and I ask you that, and I know there's a lot of football fans in the area and you probably work with quite a few, but I ask you that because I want to make a little comparison here today on the podcast between football and finance, a little term called the Financial Red Zone. So if you're a football fan at all, you've probably heard the term Red Zone, you know the term Red Zone. It's the 20 yards out from the end zone in and it's one of the most critical areas in football. Your offense needs to execute, if you can turn those Red Zone appearances into touchdowns, you have a much better chance of success, and if you're a defensive team, if you can make stops there, obviously it's a big deal, but it's about execution in this area. It's a critical point and much like that, there's the Financial Red Zone in retirement.

It's a critical time as well to help determine your success. So today we're going to kind of make that comparison, talk about it a little bit, talk about some of the mistakes people commonly make here in this area and go through this completely. So if you have questions today after we get done discussing this, again, you can log on CravitzFinancial.com is the website. You'll find Ryan and his team there, but if you want to call, you can do so as well. It's (714) 462-9155. All right, so this term Financial Red Zone, maybe some people have heard of it, maybe they haven't. But as we throw this out here, Ryan, what exactly does it mean?

Ryan: So the Financial Red Zone or retirement Red Zone is that time period, which is generally about 10 years right before you retire, up until about five to 10 years after retirement. And as you're describing with football, this is a very critical time period in the overall retirement planning process, if you will. And what I mean by retirement planning process is I look at it as that there's three phases of money. You've got the accumulation stage, the preservation stage, and then you have the income phase. So the accumulations typically when you're in your twenties, thirties, forties into your fifties, and then generally sometime in your mid to late fifties, you start to get into that preservation phase. For a lot of people, that's when they're going to be about 10 years away from retirement. And then of course the income phase is when you're retired and you're no longer working, you're no longer getting that paycheck from your work and instead now you got to get income from all your income sources that are available to you, whether that's social security, whether that's a pension, whether that's your retirement accounts, any of that.

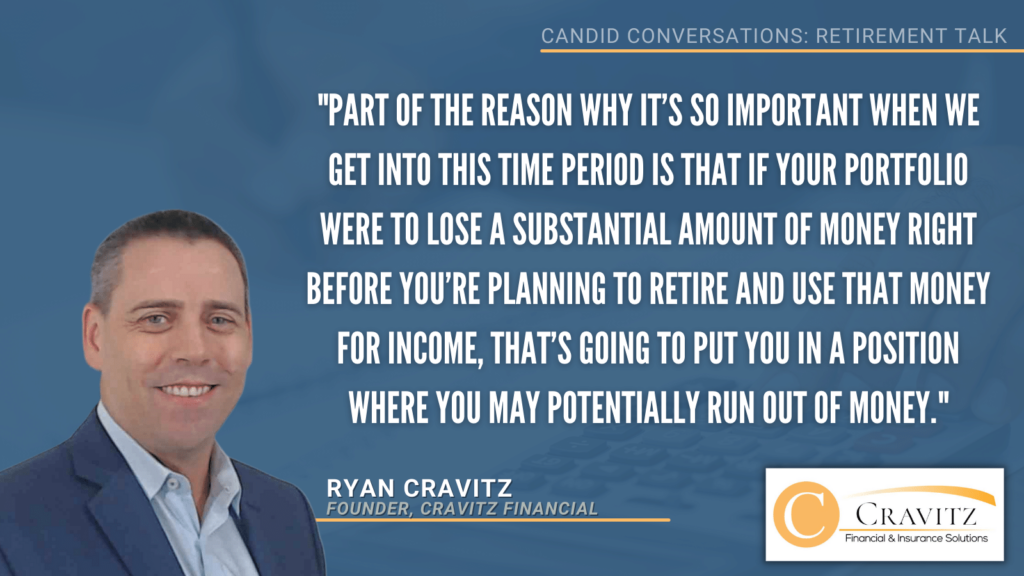

So the critical time period is that, and that retirement Red Zone again starts about 10 years before, and part of the reason why it's so important when we get into this time period is that if your portfolio were to lose a substantial amount of money right before you're planning to retire and use that money for income, that's going to put you in a position where you may potentially run out of money, or at a minimum you'll be in a position where you may very well have to reduce your lifestyle or maybe you're going to end up making the decision to delay retirement.

Too often I see this happen, that people are taking too much risk in the Red Zone. When the stock market's doing well, people are investing. And quite frankly, if you've been in the accumulation stage of life, you're not really thinking about that transition into preservation and then into income. It's all about just saving and investing for the future. And over the last several years, we've had some pretty good stock market years or years in the stock market. And now, if you're going to need to use that money and your retirement savings for income and that money drops substantially right before you need that money for income, that could be a real big problem for you in retirement.

Ben: Yeah, and it makes a lot of sense why it's so critical. So as you look at this, it just sounds like the reason why you want to pay more attention here, and if you're not already and you're in this Red Zone, you want to listen here closely because time is no longer on your side, that's the biggest thing. There's just not room to recover. That sounds like that's the biggest factor here.

Ryan: It is, and it also doesn't mean that you take all risk off the table either.

Ben: Right.

Ryan: And so, I see this on two extremes as an example, a lot of people that I have talked to in the past have been taking too much risk, I'll see in their 401K plants. And especially when the market's doing really well, they may see their 401k continuing to grow and everything seems...

I remember talking to a guy about a year ago and he was planning to retire in about a year from then, and he looked at his 401k statement, he liked the balance also on his statement, it would show what his potential income would be in retirement based up on that account balance, and he was feeling pretty good about it. The unfortunate thing though that happened to him and I think happens to a lot of people is that they're not thinking, "Well, okay. Yeah, the market's been great recently, but what if we do experience a big market pullback?

I mean every few years or so we have a bear market and a bear market is a 20% loss, and if all of his money is invested like it was invested in that 401k plan and he needs to use that money from that 401k to live on in retirement, and if that money went down substantially, like for instance this year in 2022, we're having a bear market.

And I don't know what happened to him, but if he's now retired and he's lost this much money in the market, that's that's really hurt how much he's going to be able to live on. And the other side of the coin here, I mean, that's somebody that was certainly taking way too much risk. He didn't have what I call short, medium, and long-term money and a real plan built out, which I'll talk about here in just a second, but on the other side of this, I see people that get close to retirement, they're in that Financial Red Zone and they start thinking, "Well, I can't invest like I did when I was 35, I'm 65 or 70" or something like that, "I need to be much more conservative."

And I will say that when I construct retirement income plans, because most of the people that I talk to are in that retirement Red Zone, what I find is absolutely critical is to make sure that you have your short term, your medium term, and your long-term money. Even if you're 65, 70, even 75, you likely need to have long-term money as well, because when I break it down, short term is typically money that you're going to need to use either now or sometime in the next year or two.

Ben: Okay.

Ryan: And that money is not subject to any market fluctuation. It's stable, it's highly liquid, it's available to you at any time. And then we've got the medium term money, which is money that you're going to need in the next two to 10 years, typically. It can vary person to person, but that money might be subject to a little fluctuation, it might not be subject to any. And then you've got the long term money. And the long term money is typically money that you won't need for 10 years or more, and the reason it's so critical to do that is if you're retiring right now and the market over the course of that next year takes a big dip, a big loss, and you're taking income from that portfolio at the same time, that puts you at very real risk of running out of money. But if you know, "Hey, the money that I need in the next year or two or three or four or five, that's the money that I'm going to tap into for my short term and medium term money."

So, if you look at the news and they say, "Hey, the Dow Jones just dropped 800 points" you really don't have to worry about it. I mean, the media really loves to get excited about some of that stuff, but if you're in a position, right? And you have a proper plan put in place, and you have that short, medium, and long-term money, yeah, you're going to have those ups and downs in the markets and we have bear markets every few years or so, and so what if that affects the long-term money? That's okay as long as everything is put together and we know exactly when we're going to get our income from what sources and when.

Ben: So we also talk about being proactive and a lot of things that we do, Ryan, and same can be said with our finances, I know it's always easier to prepare for retirement and put money away if you start early and you get ahead of things. You can maybe get ahead of potential issues, make adjustments earlier. So for anybody that's been proactive in this with their money and managing it, why is this an easier time for them in the Financial Red Zone rather than someone that maybe doesn't think too much about their financial planning until they arrive here?

Ryan: I think some of the reasons why it's definitely easier is because you probably have a retirement age in mind. When you're years away from retirement, you don't know when that date is actually going to be, but as you get closer, you likely have a retirement age in mind. You likely know what you're going to get from Social Security or at least thereabouts about how much you're going to get, if you're entitled to a pension, you about how much you're going to get there. Also, for a lot of people, you're likely out of debt or at least you're at a point where you're seeing the light at the end of the tunnel. Maybe you just have a mortgage and you're continuing to pay that down, but really you just have a much clearer picture of what you want to do with your life once you retire.

Ben: So again, if you could start earlier, the better, right? That's what we always want to pay attention to, but it's okay if you haven't, right? I think for people that haven't started yet and are approaching the retirement Red Zone, this is a great time now to really focus in and do that. And I know you have a lot of experience in this area too, right Ryan? Because you've been doing this obviously for over 20 years, but the people that you work with the majority of the time are people over the age 50. So I'm guessing a lot of people are either getting close to this Red Zone or in the Red Zone when they come to work with you.

Ryan: Yeah, most of them are in the Red Zone that I find, and I would say the crazy thing is, or the hard thing is that it could be a difficult transition going from that accumulation stage into the preservation and then finally into income. Because for so many years our focus is just on accumulating money for the future and we're working, so our paycheck is coming from our job and meanwhile we're continuing to save and invest in our various retirement accounts, maybe automatically it's coming out of our paycheck, and so the focus there is our income, again, is it is all coming from our jobs.

But now as we start to get into that preservation phase and now we've accumulated, for most people, the most money that you're likely to have ever, you kind of hit the top if you will, you kind of reach that top of the mountain. But now as you close in on the top of the mountain there, so to speak, now it's about, "We've got to get down the mountain" and we've got to get down that mountain carefully and we've got to utilize everything that you've accumulated so far efficiently. And it's hard I think, sometimes for people to make that transition, "Okay, I've been focusing on accumulating for this long, I'm going into preservation and now I'm going to actually spend this money." And for a lot of people it can be fearful, because if you're in your sixties and planning to retire thereabouts, you could very well live another 20 or 30 years in retirement and having a game plan put together so you could feel confident in the lifestyle that you want to be able to live all throughout your retirement years.

Ben: Well that's the goal. That's what we want to accomplish, and that's why you work with a financial advisor to set you up for that. So, if you're getting close to the Red Zone, that five to 10 years before retirement and haven't done so, take the time now to sit down with an advisor, if you want to work with Ryan or at least have that first meeting to meet him and maybe do your retirement ready checkup, you can always find him online. CravitzFinancial.com is the website, but also the phone number is (714) 462-9155. Again, confidence, security, peace of mind, that's what Cravitz Financial is all about and that's why we wanted to talk to you today about the Financial Red Zone. So good stuff, Ryan. I know that there's a lot of football fans around, so hopefully they make that connection next time they watch. But more importantly, hopefully you're paying attention to these five to 10 years before retirement.

Ryan: No doubt about it.

Ben: Well, I appreciate your time today. Thank you for listening to Candid Conversations Retirement Talk with Ryan Cravitz. I'm Ben George, he's Ryan Cravitz over at Cravitz Financial. We'll talk to you in the next episode. Take Care.