Mentioning taxes is usually enough to turn people away from a conversation, but when you put some thought and strategy into how you approach your investments, taxes can actually work in your favor.

Tax planning is another core piece of a comprehensive retirement plan so let’s focus in on this area. People often confuse this topic with tax filing, but when we say tax planning we’re talking about what we can do in order to increase our after-tax, spendable income. Making the right decisions with your investments today can help you keep more of your money down the road in retirement.

Here’s some of what you’ll learn on the podcast:

- The difference between tax filing and tax planning. (1:19)

- Why you shouldn’t assume that taxes will automatically be less in retirement. (2:40)

- Strategies you can use to improve your tax situation down the road. (5:50)

- Tax planning tools to have more control over your money when you’re gone. (7:18)

- A story about a tax planning strategy we’ve used with clients in the past to make a big difference. (9:39)

Thanks for listening to this episode. Please get in touch with us if you have any questions about your financial plan.

Full Transcript:

Ryan: We're talking about long term, what we can do in order to increase our after tax spendable income.

Announcer: When it comes to financial planning, you need to cut through the jargon so that you can understand how to achieve your own retirement success. This is Candid Conversations: Retirement Talk, with Ryan Cravitz of Cravitz Financial & Insurance Solutions.

Ben: Glad to have you back on Candid Conversations: Retirement Talk with Ryan Cravitz. I am Ben George, he is Ryan Cravitz at Cravitz Financial in Irvine, California. We are talking today about tax planning. And it's a great topic, I think, right now, Ryan. I know tax planning's always something that's at the top of your list as an advisor when you're working with someone. But I think kind of with tax rates where they are and everything, that now is as good a time as ever to really be honing in on how you can be most efficient, how you can get everything in order. Because most people aren't thinking that far ahead, are they, when it comes to taxes?

Ryan: No, absolutely not.

Ben: So it should be a good show today. Again, I'll point you to the website, CravitzFinancial.com. And if you have questions, you want to follow up on anything tax related, or if you just want to get some eyeballs on your financial plan or start one for yourself if you haven't done that yet, you can always call (714) 462-9155. So most people assume when you hear the word tax planning, they think, "Okay, April 15th, I've got to get my taxes done and sent in to the IRS so they can go through that." But that's not what we're talking about here, Ryan. What's the difference between that tax filing and then tax planning?

Ryan: That's a great question, and you're absolutely right. Everyone that thinks about tax planning is usually thinking of late January, I get these different statements in the mail, 1099s, all that. You're putting together your tax documents, you got to get that done by April 15th. But what we're talking about is tax planning, or what I like to say is tax forward planning. And that's really about planning for the next, let's say, 20 or 30 years, and what are we going to do in order to minimize the taxes that you have to pay over that course of time.

Tax filing is about just looking in the rear view. There's not a lot that you can do after the year is up. Maybe able to contribute to certain retirement accounts like an IRA and get a tax deduction. But you're limited in the options that you have there. We're talking about long term, what we can do in order to increase our after tax spendable income.

Ben: I wonder if for people that aren't thinking as much about tax planning, I wonder if it's because a lot of people do assume that their taxes are actually just going to go down in retirement. You're not going to have to pay as much, you don't have a regular paycheck coming in, but how often are people actually right about that?

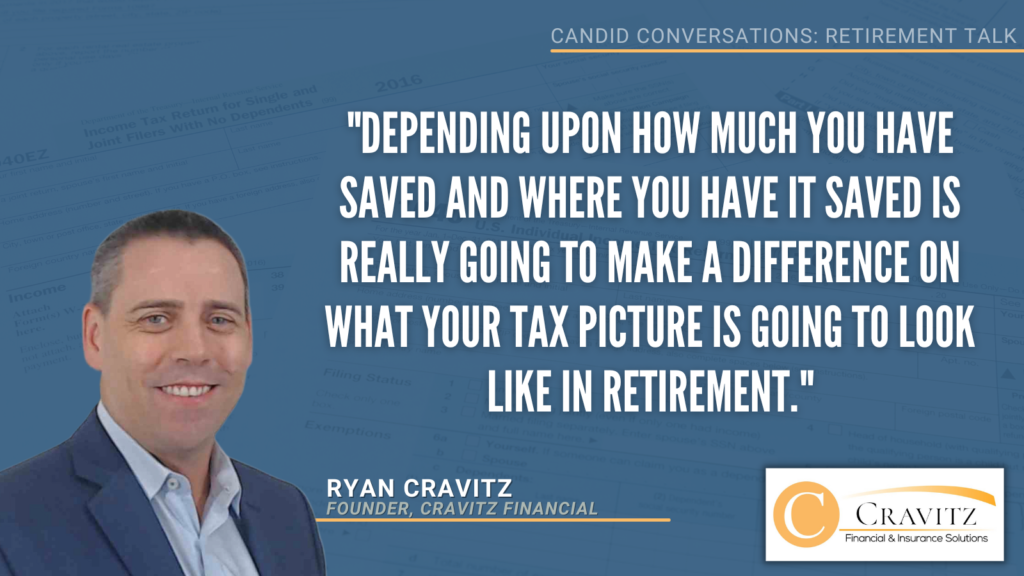

Ryan: I mean, for some people it's definitely true. Their taxes are going to be less. I mean, you're no longer paying payroll taxes like you were when you're working. And so depending upon how much you have saved and where you have it saved is really going to make a difference on what your tax picture's going to look like in retirement. So I've seen situations on both sides here. On one side, for some people, they've done such a great job of saving and investing in their 401(k) plan and they're putting the maximum in there. They're getting the tax deduction today, which it's all good, but then they get into their retirement years and I've seen people that have had multimillion dollars in their retirement accounts that are all going to be subject to ordinary income tax when they go to withdraw from these. And for some of those people, they may very well be in a higher tax bracket.

The other thing that people don't really consider is that by the time you get to be age 72, there's a mandatory amount that you're going to have to take out each and every year. And for a lot of people it's even more than they would want to take out. But the IRS makes you take it out because, well, it's never been taxed. They want to get their tax money. So unfortunately there's a lot of situations where I see there where we're doing a good job on the investment side, but the future tax forward planning is really not thought through. And then the impact that that has not just on taxes, but also could potentially make your Social Security benefits taxable when they may not have been or more taxable than they would've been otherwise. It could also make you have to pay more for Medicare due to IRMAA. So there's some things there.

But then on the other side, I've seen situations where somebody came to me and he said, "I really want to do a Roth conversion because I want to make sure that I have tax-free money in retirement." And I ended up telling him that I didn't think it was a good idea and we went through the numbers as to why. And really based on his situation, he was going to be in a pretty low tax bracket in retirement.

So as you can see, for some people their tax rates probably will be higher and other people, it probably will be lower. Now having said that, I definitely do believe that overall tax rates will go up in the future, but that doesn't necessarily mean that you'll pay more in taxes. So it's definitely a case by case basis.

Ben: Yeah, that's a great point. I think when you talk to anyone or listen to anyone, I guess, everyone seems to indicate that taxes probably have to go up from here to cover a lot of the spending that's happening right now within the Fed. So it makes a lot of sense. But that's good to know that doesn't necessarily mean you will have those extra expenses as well. So for anyone that maybe is concerned and hearing that and saying, "Okay, I don't know for sure what my taxes might look like and I haven't really thought a whole lot about it," what are some of the strategies someone can use while they're still working to improve their tax situation down the road?

Ryan: Well, one of the things that they can do that a lot of people overlook is a lot of companies, where people work, if they've got a 401(k) plan, they may also have an option for a Roth 401(k). And if they do, you may want to look into that and you may want to contribute maybe some money into the pre-tax 401(k), but you may want to contribute some money into that after-tax, that Roth 401(k) as well. So that's one thing.

Another thing that people could consider doing is considering whether it makes sense to do Roth conversions. So that's something that I like to look at on an annual basis and see if it makes sense to convert any money. And without getting into the weeds on that, that's simply taking money that's, let's say, in an IRA. And when you convert it to a Roth IRA, you have to pay taxes on the amount that you convert in the year that you do the conversion, but in the future that money in the Roth IRA, you'll be able to access that tax-free. So those are some of the things that I would consider doing.

Ben: Okay. Well, again, if you haven't looked into that, please do so. It could be an option that works well for you down the road. Also, with taxes when you're looking at planning for someone over time, I think a lot of people are looking at ways to maybe have the most efficient control of their money even when they passed. So are there some ways that people are able to do that to kind of have a little more control over their money once they're gone?

Ryan: There's different tools and strategies that you can use here. One of them is the Roth IRA. Another one is life insurance because when money passes to the beneficiary, it passes income tax free. So that's another one that can be utilized a lot. In fact, sometimes what happens is that I see, some people, once you reach 72, you have to take the required minimum distribution. So there's a certain amount that you have to take out of your qualified plans each year. And for some people, again, they don't need that money. And I've seen some people will take some of that money and some even all of that money and fund a life insurance policy. And they'll use that money just to fund the premium each year and when they ultimately pass away, that money can get passed on to the next generation, their children or grandchildren or whatever they prefer.

Ben: And I mean, we work so hard to save money and you spend so much time and effort to save that you want to be able to pass as much on as you can. I know that's important for a lot of people to have that legacy. So some things to think about there for tax planning as well. Are there any examples that you could think of, of a tax mistake that you've seen people make with their investments that had they come in and sat down with you or sat down with an advisor beforehand, they could have avoided altogether?

Ryan: Well, one thing is, I was talking to somebody the other day and she was younger and she was funding her traditional IRA and her income was pretty small. Again, she's younger, just getting her start in her career. And I was talking to her about a Roth IRA and how that worked and that she might actually benefit more by funding a Roth IRA because she wasn't paying a whole lot in tax now. But her plan was to be a doctor and her income would definitely be going up in the future. So might as well pay a little bit of tax now and have that just continue to grow tax free.

Ben: Very good. I like that. Tax planning, again, as you can see, can save you a lot over time and it's such a key piece. And again, this is one reason why we with this route for episode number three in the podcast. Maybe we could finish off maybe with a story here on a tax planning strategy that you've used in the past to really help make a significant difference in someone's retirement plan.

Ryan: So one of the things that can make a big difference, and it's something that I like to take a look at towards the end of the year, is whether it makes sense to do any Roth conversions. Because for some people, we talk about diversification all the time when it comes to investments, but if you ask me, we don't talk enough about diversification when it comes to taxes and tax forward planning. And there just isn't as much thought given to how are we going to plan for in the future, what money we're going to withdraw from and where we're going to withdraw. It's just, again, like we were saying, it's just about accumulating and seeing whether it makes sense to do any Roth conversions on an annual basis.

And if it does make sense to do it, how much to do makes a lot of sense. Because when you're thinking about your income plan and you're thinking about what money you're going to withdraw from where, there's a lot of flexibility that a Roth IRA has in retirement because there's no RMDs, there's no required minimum distributions. So if you don't want to withdraw from it during your lifetime, you don't have to. You can continue to let that grow. And so there's a lot of that flexibility that's built in by doing that.

Ben: Yeah, that's a great thing to keep in mind. And depending on what time of the year you're listening, we're recording this as we kind of are closed down on the end of the year. So I know you're thinking about us a little more top of mind than normal. But something to ask your advisor no matter what time of the year you're in, if a Roth conversion makes sense for you, something to maybe explore. So some good information. Again, as you can see, tax planning is crucial. It's critical to long-term success. And I know it's tough to come off some of that money now and knowing that it's going to pay you off later. It's always tough to kind of cut that check early. But hopefully this will help you understand that there is some big benefits to doing tax planning now for your retirement.

So if you have questions, if you want to follow up on anything, you can always do so at CravitzFinancial.com. That is the website there. You can get in touch with Ryan that way. Or you can call him directly at (714) 462-9155. I know nobody loves talking taxes, but it is so important, Ryan, and I appreciate you taking us through this.

Ryan: Absolutely. Thanks, Ben.

Ben: Thank you for listening to Candid Conversations: Retirement Talk with Ryan Cravitz. I am Ben George. Thanks for listening. New episodes coming in a couple of weeks. Hit subscribe and we'll talk to you then.